If it seems like your money is burning a hole in your pocket on the 1st and 15th of every month, you might benefit from some budgeting tips for military families.

Unfortunately, personal finance isn’t a skill that’s taught in school. It’s basically a learn-as-you go life skill that most people figure out after they’re already swimming in debt.

But that doesn’t have to be you.

While you may have a steady paycheck, that means you also have steady bills, too. If you’re ready to learn how to be financially smart, you’re ahead of most people. And that’s exactly how wealthy people get ahead — by learning how to manage their money.

Best of all, as an active duty military member, you have access to free financial counseling and classes to help you learn how to be smart with money. Need a primer? Below we’ve included some tips and insights on managing your money well while you serve.

If you’re not sure where your paychecks go, this post is for you.

Budgeting for Military Tip: Financially smart service members get ahead

When you’re not stressing out about money, it means you can focus on other more meaningful life events, like enjoying quality family time or getting a promotion. If you make your money work for you instead of against you, it makes everyday life more enjoyable.

Create your detailed 2020 financial plan today. Then stick to it.

Not sure how to get started? Here are a few ideas:

- Check out your library’s financial section – First things first, be thrifty and get FREE books from your library. Educate yourself on personal finance, debt elimination, building wealth, etc. in your free time.

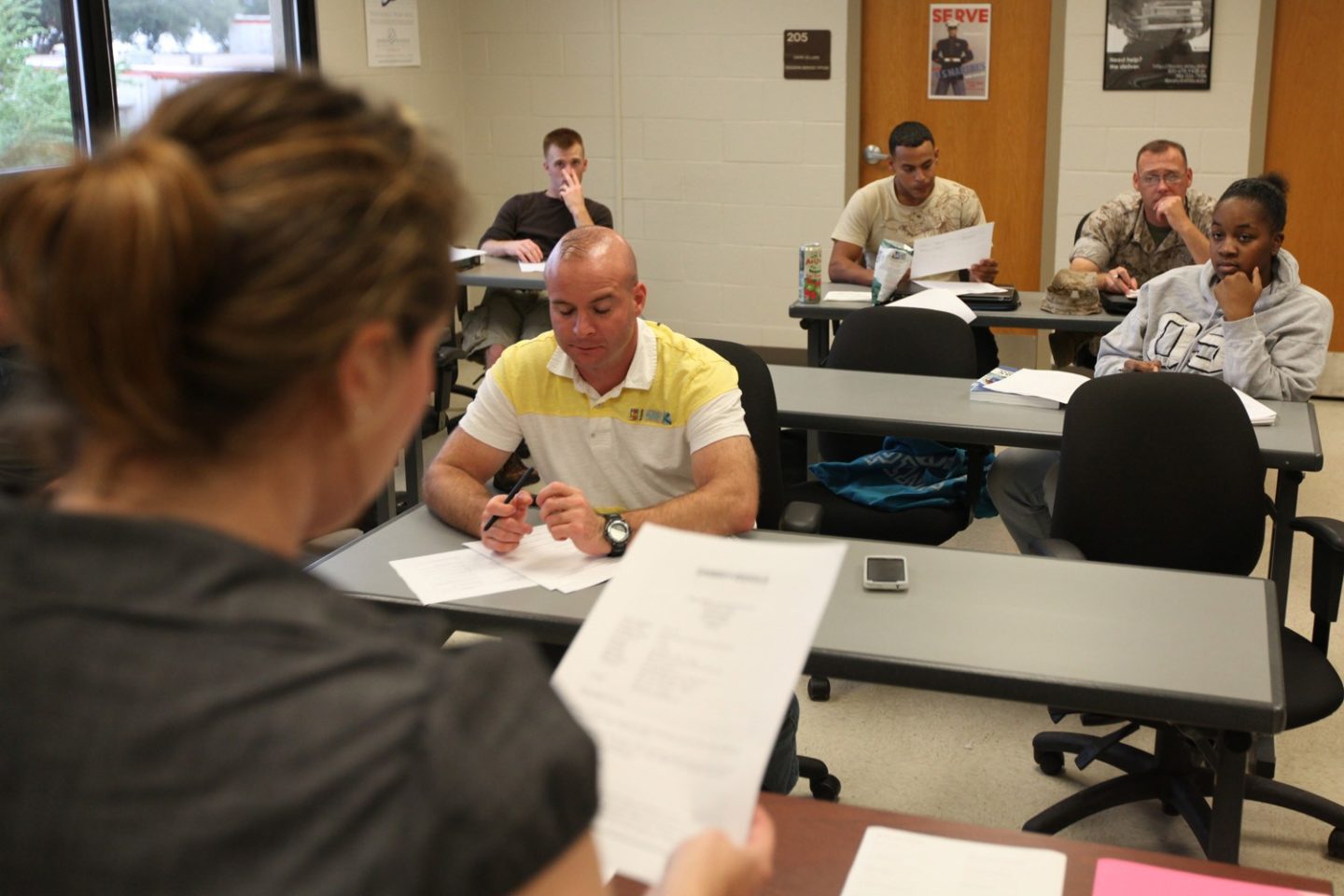

- Meet with a financial counselor – You get access to a lot of fantastic resources as a military member. Take advantage of meeting with financial counselors on base. You can also chat with someone on Military OneSource as well.

- Take a financial class – On top of having access to a financial counselor, most bases also offer personal finance classes, too. Take one to learn about budgeting, credit cards, paying off debt, etc. Financial Peace University is another way to learn personal finance.

Curious about personal finance and how it applies to your service life?

Here’s an overview of how to be smart with money as an active duty service member:

Budgeting for Military Tip: Pay takes a while to kick In

Now that you have a signed contract, you should get your first paycheck soon, right? Not so fast. You don’t get to spend those Benjamins right away.

When you’re in basic training, you don’t have much time to spend money, anyway. But you will pay for some necessities as your paycheck gets docked for supplies like uniforms and other basic training essentials.

Save a few thousand dollars, if possible, before you head into training.

Money-saving boot camp tip: For any bills you have back home, make sure you put them on auto pay or have a trusted relative take care of it while you’re away. Doing so will ensure you won’t be greeted with overdraft or late fees upon graduating.

Learn more about the 2020 pay charts here.

Budgeting for Military Tip: Take care of your money

If you’re smart with your money, it will take you far. That means living below your means, making wise investments, and creating a monthly budget. It’s not hard, it’s just a matter of discipline.

Budget

Creating a monthly budget is one of the first tasks to learning how to direct your money instead of letting it run your life. Sure, bills are an inevitable part of life, but planning for payments can make the process painless.

How to do it:

- Get your spouse on board if you’re married

- Track spending to see where money goes

- Use cash instead of credit cards

- Pay off debt (smallest debt first!)

- Create a savings fund

Budgeting doesn’t need to be complicated. In fact, a note on your phone, an Excel spreadsheet, free money apps, or a piece of paper all work fine. The goal is to learn exactly what expenses you have and how much money you need to cover those expenses.

Save

Just as it’s a must to pay your bills, it’s also important to have a rainy day fund. Saving leftover funds for emergencies, future events, and eventually retirement gives you confidence that your needs will be taken care of due to diligent financial planning.

How to do it:

- Set up automatic savings withdrawals

- Get rid of debt

- Buy generic (yep, skip name brand!)

- Put any extra money into savings

- Keep a separate retirement account

Once you have a solid budget in place, you’ll find out where your money is going. Because a good budget has a line item for each of your living expenses, you’ll be able to see where you may be spending with reckless abandon. That, in turn, makes you more mindful about spending habits and allows you to save money.

Budgeting for Military Tip: Don’t blow bonuses

Whether you have a sign-on bonus or a reenlistment bonus, there’s no need to spend it all in one spot. If possible, save most of it and spend the rest on essentials. Plenty of service members get excited by fat bonus checks and head straight to the car dealership.

Instead, consider the following:

- Pay off debts

- Build an emergency fund

- Invest in your TSP

- Save the rest

You can and should use your hard-earned bonus, but use it wisely. Bonuses are few and far between, so it’s important to use the funds appropriately to maximize the benefits of receiving one.

Budgeting for Military Tip: Don’t use BAH for magazine-worthy living

Basic Allowance for Housing (BAH) adds extra funds to your paycheck to help cover living expenses. This rate is based on a variety of factors including geographic duty location, pay grade, and dependency status. This rate coincides with the cost of living in local civilian housing in the U.S. if base housing isn’t available or provided.

A few tips to find safe, affordable housing:

- Check out AHRN.com – This site allows you to search for homes by military installations. You can also post a home you want to rent to another military family or service member.

- Search MilitaryByOwner.com – Created by a Marine Corps vet, this site is for military families looking for, selling, or renting homes near military bases.

- Look on HOMES.mil – This Department of Defense (DoD) site helps families locate housing rentals near military bases. You can also list your own property at no cost.

If you’re not planning to live on base, you’ll need to find affordable housing in the area. The military can’t dictate where you live off base, so it’s important to do research and find reputable communities to live in.

That means you can live in as expensive of an apartment or house you want to, even if it goes above your BAH. But that doesn’t make it a smart money move.

Prepare for Irregular Income Periods

Income may be irregular, like when you get that unexpected uniform allowance or a pay boost. But then you forgot that they overpaid you three paychecks ago, so this week’s paycheck gets docked. Having some extra savings set aside can help in these instances.

Budgeting for Military Tip: Create a PCS Move Fund

Even though the military pays to relocate you during a PCS move, it’s still pricey. You may have some upfront costs that you’ll be reimbursed for, but it’s still money out of your pocket you’ll need to account for as soon as you get new orders.

Some costs that can add up during a move:

- Relocating pets – You’ll pay extra for pets when staying in hotel rooms. Not to mention any extra vaccines, medicine, etc. you may need to stock up on before hitting the road.

- Privately owned vehicles (POVs) – Not planning to drive your own vehicle to your next duty station? You’re 100% responsible for the cost of shipping it.

- Car maintenance – If your car breaks down along the way, you’ll need to put it in the shop ASAP to make it to your new duty station for reporting. This can be costly depending on your location, parts and repairs needed.

- Replacement of household items – Movers break stuff, unfortunately. You may get to your destination and realize your vacuum is broken and won’t turn on. You’ll need a new one right away, so it’s good to have some cash set aside to replace broken or lost items. You’ll usually be reimbursed, but it takes time (and proof) to get the money back.

You can plan ahead for a PCS move. It’s no surprise that you’ll move around when you’re in the military, which is why creating a savings plan for events like PCS moves is a critical money move to make.

Budgeting for Military Tip: Look at investing for retirement

Retirement is much closer than you think. As the saying goes, “the days go slow and years go fast.” Starting to prepare now and contributing toward an appropriate retirement fund will ensure you spend your Golden Years relaxing instead of working.

Three options to consider:

TSP

The Thrift Savings Plan (TSP) is a retirement savings and investment plan that you’re eligible for as a service member. It’s a contribution plan and an easy way to save for retirement without putting much thought into it. Check out the benefits of TSP enrollment here. You can choose between pre-tax and after-tax deductions for TSP.

Roth IRA

This is a tax-advantaged, retirement savings account that allows you to pull your money out in retirement years tax-free. It’s a future bonus that if you contribute now, you’ll keep all the money when you pull it out in retirement. You can also continue to contribute to it well past your retired age.

Traditional IRA

A Traditional IRA allows for make pre-tax contributions. While you’ll get an immediate tax benefit now, you’ll be taxed at your current income level after age 59.

Be Thrifty

When you start budgeting and saving, it’s easier to get out of the “I want it now!” mindset. You get intentional about where you spend your money, which generally leads to overall better financial decisions — including being thrifty. Some general ideas on being frugal:

Enjoy cheap date nights

Going out to a fancy restaurant and a movie is lovely, but it’s also expensive. Consider thoughtful yet fun options that are cheaper:

- A picnic at a local park

- Rented movie and dinner at home

- Game night at home

- Free local attractions

Bases always have events going on, too, like movie nights, festivals, concerts, and more. Check your installation’s events calendar to see how you can save money but still have fun!

Pack your lunch

The average American household spends about $3,459 on food outside the home, according to the Bureau of Labor Statistics. While buying lunch a few times a week seems more like convenience, it adds up quicker than you might think. Pack your lunch and watch your savings grow!

Savings tip: Shop at the commissary to get your groceries tax-free and score deals on brand name items, too. Plus, you can use coupons!

Use your military discount

Lots of military towns support service members who patronize their shops, restaurants, and businesses. Anytime you’re out and about, ask at check-out if the business offers a military discount. You’d be surprised how much you can save!

Remember: Being thrifty doesn’t mean you have to stop having fun, but you get more creative with how you keep more money in your pocket.

Check Out Your Education Benefits

One of the biggest perks of post military life are the educational benefits. The GI Bill is probably the most recognizable benefit. It can help you pay for college, training programs, or graduate school.

If you plan to use your educational benefits once you’re discharged from the military, it’s good to use the U.S. Department of Veterans Affairs GI Bill comparison tool. This will help you decide which benefit is best for your current circumstances.

Choosing the right program for your situation and post-military career goals can save you thousands of dollars on education costs, including tuition, books, and more.

Budgeting in the Military is a Must

With so many unpredictable lifestyle factors in the military, being financially smart can alleviate some of the lifestyle stress.

Living paycheck to paycheck doesn’t have to be a reality. When you take control of your budget, save, and say no to unnecessary spending, it puts you in the driver’s seat for your financial journey.

It’s how you spend and save your money that really matters. So make the budget, talk to a financial guru, or take a class. Do whatever you need to do to feel financially savvy when it comes to your personal finances.

The path to financial wellness is one you get to do on your terms. Using the tips above is just a starting point for learning how to be smart with money.

The rest of your financial journey is up to you.

Deploying soon? Learn how to Make Your Money Work Harder For You While You’re Deployed!

Feature image courtesy of the Dept. of Defense